- MoneyBits

- Posts

- Chevron

Chevron

A precedent, dollars for everyone, being patient, and lack of talent.

Listed Reserve

July 05, 2024

📚️ PDF ⏳️ 7 min 📖 8

Chevron

I confess to never having heard of the Chevron Precedent. Certainly though, as an industry, we have been held back by its consequences. The 1984 ruling gave federal agencies wide powers to interpret the law, including how they might best be implemented. Previously when challenged, Federal Agencies have simply pleaded “Chevron”. The US Supreme Court has now overturned that by 6 - 3.

Happily, this whole thing was not brought to a head by some mega-corporation that wants to drill for oil in a polar bear sanctuary but rather by some aggrieved fishermen from New England.

In this case, the National Marine Fisheries Service required a group of commercial fishermen to pay the wages of monitoring programs to ensure they were complying with conservation laws. The original statute did not specify that the wages must be paid by the government, so the government handed the fishermen an estimated cost of $710 per day.

This looks like classic rent-seeking behaviour. We dream up a law and then dream up a regulation that means you need to pay us to enforce it over you.

The best example I can give of this has been the way the SEC has treated cryptocurrency. The bottom line was (and is) that the asset class is new and has all sorts of features that don’t really fit into the current framework. The SEC then attempted to retrofit these assets into existing legislation. That is how they blocked the Bitcoin ETF for so long; it's also how they failed to provide any guidance around any innovation that the sector came up with.

Some people seem upset that Chevron has been overturned, but it seems rather sensible that you can’t just have a federal agency making it up as they go. For years the SEC (and others) have simply interpreted the rules in whatever way they liked to suit a predetermined outcome that they wanted; that era is now over. As one of the Justice’s wrote on the ruling:

The Chevron doctrine “allows agencies to change course even when Congress has given them no power to do so.”

In what looked like a very bad week for American democracy at least they got something to redress the balance. This one might be far reaching with nearly every regulation in the US up for challenge.

Fed cut rumours

In most corners of the world, the view is there is no way the Federal Reserve is cutting interest rates anytime soon. The US economy is supposedly booming with nearly every metric pointing up.

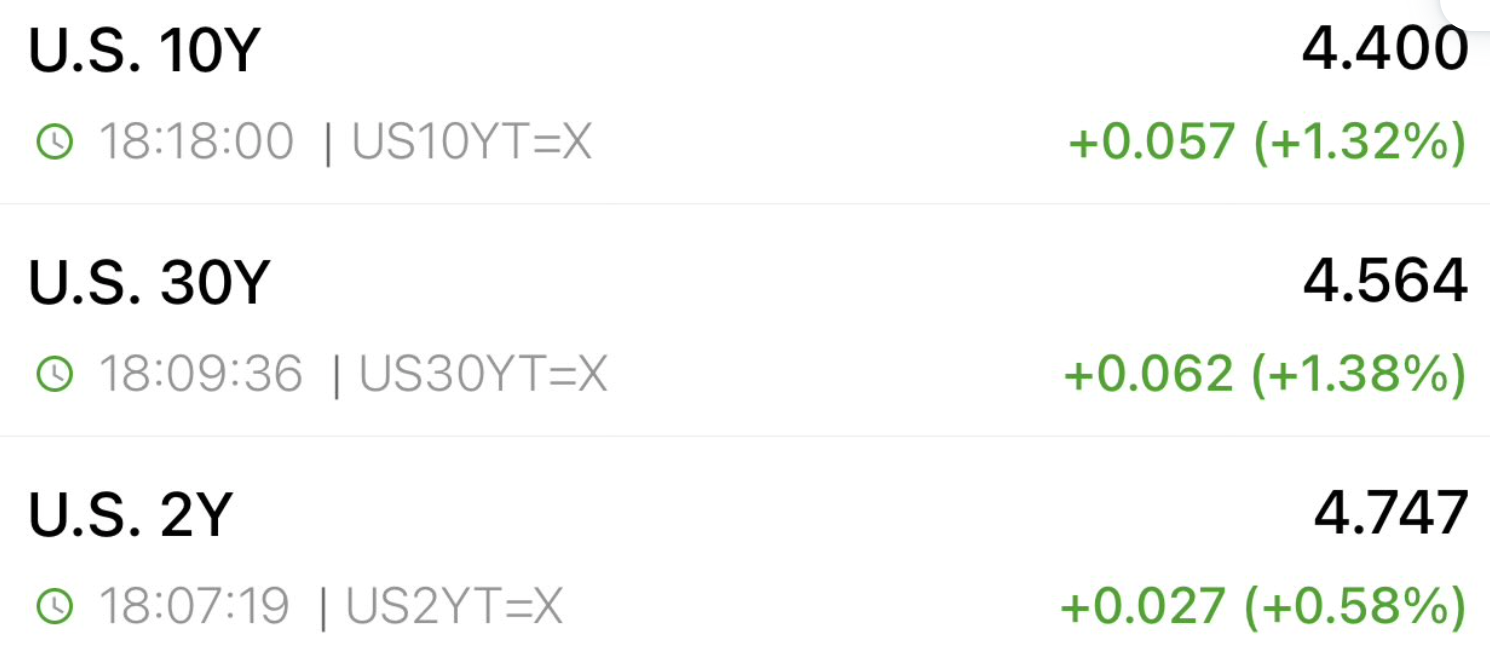

Here’s an alternative for you though. The US establishment wants a cut. The election is coming and the incumbent (who they would prefer) is clearly struggling. Yet US borrowing rates are creeping back up, with the 10 year yield racing back towards 5%, some way short at the moment but not going in the direction anyone would like.

With $34 trillion in debt (ignoring all state debt, unfunded pensions, etc.) just the raw figure interest payments now exceed defence spending and rising, more than any other line item.

It’s not so much that this is an enormous issue, more the case that the government's projections on these things are nearly always wrong and nearly always in their favour. Only one year ago they predicted that this situation would not arise until 2028 and now it’s already here.

The Americans have no money. To prevent bankruptcy they will have to print it, cut interest rates and export their issue to the rest of the world.

That is their sole privilege as the global monetary hegemon. It seems little understood that they can do this, but they can and they will and in doing so they will present themselves as helping the world. For example, unlimited money to prop up the Yen. China’s difficulties and the weak Yuan aren’t helping the US either; dollars will be heading their way. Dollars for everyone, thanks Uncle Sam.

They need to cut their rates. The market is pricing a 7% chance of a cut on 31 July. I’d say the odds are higher than that.

BNB

Another important case this week concerning BNB (the Binance native token) and the BUSD (Binance’s stablecoin). In a case brought (again) by the SEC, the court decided that secondary trading in these tokens does not constitute the sale of a security.

These decisions are hugely significant for the industry. Clearly the ICO world of marketing and selling these assets initially is a different matter; but even then for stablecoins like BUSD, there is no possibility of making a gain so it is unlikely that even in its initial issuance it could be a security.

These cases are actually crafting the landscape of what is and is not considered acceptable; undoubtedly too they are moving slowly in our favour.

Still, the majority of the SEC case against Binance survived the judge’s ruling and will now proceed to court. More to come here as we head toward a world where Coinbase serves Americans, Binance serves the rest of the world and Europe uses the digital euro powered by windmills.

On that matter, the US Marshals Service announced this week that they had appointed Coinbase as their custodian for seized assets. Is this step one on the road to nation states buying and holding?

Meme of the week (be patient)

Euro-Trash

Many of you will remember former ECB Director Board Member Benoît Cœuré. Benoît spent his final few years there telling us all just how wonderful the Digital Euro was going to be.

He is one of the peak Eurocrats of the last two decades. Classically trained in true French style at École Polytechnique, worked for a University, then the French Government, then the World Economic Forum, the Bank for International Settlements then the ECB. Now, at the peak of his powers, he heads France’s Competition Regulator. Their latest release talks about the need to “regulate artificial intelligence”.

The report is extraordinary. Right at the commencement of AI in 2021, when OpenAI released their model, Europe banned it. They quite literally killed any possibility of having a meaningful position in this industry on day one. They did exactly the same with digital assets.

Now he is complaining that one of the barriers to entry is lack of access to energy. Of course, again, this is absolutely true. AI data centres consume huge amounts of power (which is why we no longer hear so much about bitcoin doing the same).

The fact is Europe (although not France) has turned off many of its nuclear reactors in an act of economic suicide. Now they realise you cannot run the technology of the current century without an awful lot of power. China has now surpassed Europe, not only in total power (they went past that decades ago) but in power per capita.

Power per capita is the true measure of national wealth and industrial capacity. You simply cannot have all the things a modern economy requires without it. Notice it is going up in India and China; and going down in Europe and the US.

Benoit further complains about a lack of access to ‘talent’. Talent, of course, which Europe drove away. The young people just left, or more importantly because of the insanity of his policies, were never born in the first place.

In this excellent podcast earlier in the year featuring Mark Zuckerberg, he explains why the limits to AI are actually bounded not by computer chips but by energy. There simply is not enough energy in the world to power what we are now capable of.

The true measure of nations going into the future will be MegaWatt hours/Capita. Without it you will fall behind. While every other government metric is likely a fraud, you can’t make this one up (hence the overwhelming success of Bitcoin by the way; you can’t spin them up without demonstrating the cost of production via energy).

Going forward, you either have energy or you don’t. The EU, Benoît and his friends don’t have it.

Further information

Our May 2024 report to investors can be found here.

If you are considering an investment in the Managed Fund, you can apply using our online application form: