- MoneyBits

- Posts

- Half the fun

Half the fun

Gen Z dominance, the halving, voting with their feet, and a tribute to opacity.

Listed Reserve

May 03, 2024

📚️ PDF ⏳️ 7 min 📖 6

Back the trend

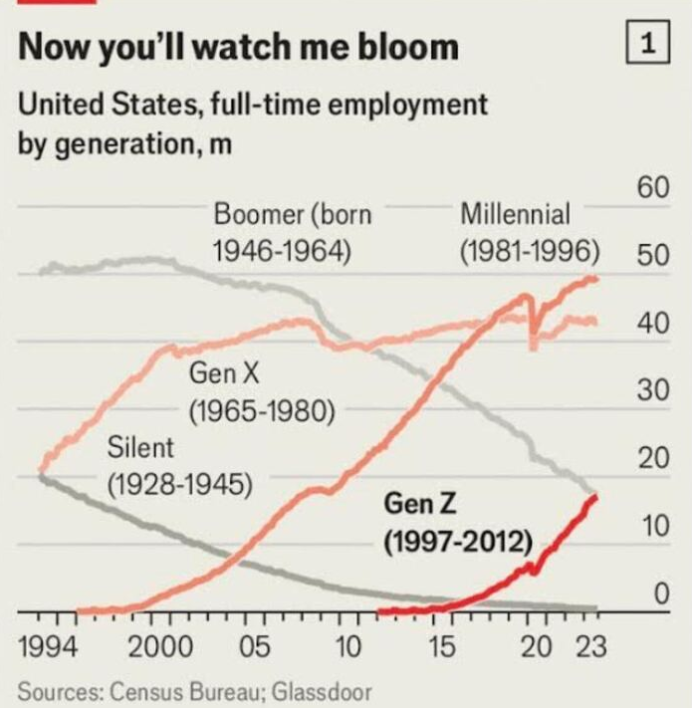

Striking chart in the Economist as Gen Z participation in the workforce passes the Boomers. There is so much of the story of the last 30 years here.

Firstly, 2008 hurt some generations. Gen X, in particular, did not recover from it. They never reached the participation levels of the Boomers before them or Millennials after them. Above all else I believe 2008 will ultimately be the point in history at which fiat currency failed. It might take another 50 years, but the point where it all went wrong will be clear to all. Not just this chart but all the others, the birth rates, the growth rates, the productivity rates and as we see above, the participation rates. Almost as though people gave up a game that was very clearly rigged against them.

Next, the dominant economic force is now Millennial and increasingly Gen Z. What they buy and consume will be the determinants of investing success. The steep Boomer decline will also be important, what will they sell to fund retirement?

Also obvious from this is how fast things happen. 5 years is a very long time at the steeper parts of the curve where Z now sits.

Stripe accepts USDC

One of the world’s largest payment providers, Stripe, has added US Dollar stablecoin USDC as a payment method. USDC (market cap $33 billion) is operated by Circle, a US business backed by Goldman Sachs, Blackrock and others. Stripe is now a huge listed business processing funds for Amazon, Apple and others. Not much happens there without US government approval; so it is telling that a stablecoin has been added and it's no surprise that a US owned and controlled version has been selected.

There is a crucial difference among the US dollar stablecoins on the market. USDC is backed (100%) by money market funds and U.S. Treasury Repurchase Agreements (which means overnight lending in the money markets) as well as some short dated treasuries. It is very much a bank style, SEC registered institutional player.

By contrast we have USDT, the offshore stablecoin known as Tether. Its reserve structure is different, comprising almost 100% US Treasuries. It has almost zero exposure to US banking infrastructure, is not SEC registered, but is a much larger player (market cap: $110 billion).

Contrary to general opinion, stablecoins are very good for the US dollar. They are not a competitor, as they are often touted to be, because they generate demand for dollars. Indeed, they are far more useful in many cases than actual dollars.

Both of these players survived the huge collapse of 2022. Tether managed extreme redemptions during the period with almost no issue. USDC had its difficulties during the collapse of Silicon Valley Bank but they both survived extreme redemption tests. Importantly, almost no bank could have survived equivalent redemptions (withdrawals). Tether lost 20% of their funds to withdrawals in the space of a few weeks. By way of example, the Commonwealth Bank of Australia, which is extremely well capitalised by international standards, has a tier 1 capital ratio of 12.2%. Were they to suffer a Tether-style shock, they would be unlikely to be able to handle it without RBA assistance.

As time passes and the stablecoins get more robust they are far more likely to attract deposits than banks. It sounds crazy to think that we might prefer to put our US dollars with Tether than with a bank. Objectively, because of the quality of reserves, there is no comparison in terms of monetary risk. The risks are actually political ones.

The halving

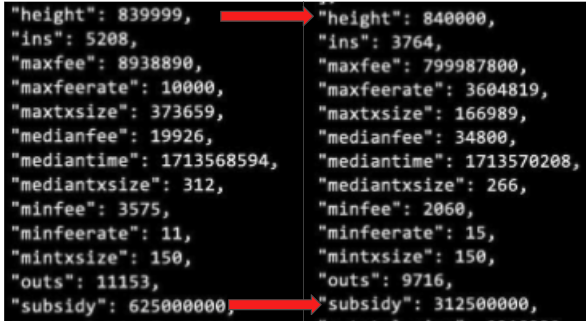

It came and it went and you are most likely disappointed because “nothing happened”. Except something did happen. Here is the output from our Bitcoin Node. At block height 839,999 bitcoin paid a subsidy of 625,000,000 satoshis (6.25 bitcoin). In the next block, 840,000, it paid 312,500,000 satoshis.

It probably isn’t that exciting except there is no other currency in the world with a monetary policy so explicit, so politically immune and so consistent. It simply does what it was programmed to do in 2009 and it will continue doing it.

Perhaps more significantly, the halving block itself generated $2.6m in fees. It was genuinely scarce digital real estate.

Don’t want to

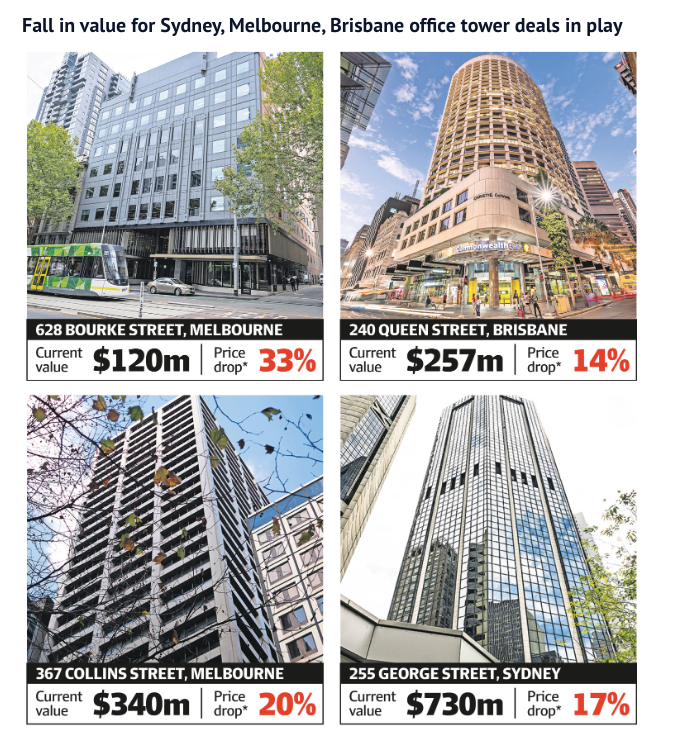

This image was extracted from an article in the AFR last month which declared “Office values plunge as CBD market bottoms”. Before I begin I should state that I don’t know that much about commercial real estate. But, I do know the building in the bottom right corner.

That is the former headquarters of NAB. Outside of that building was a vibrant food court with at least 20 different eating options. That count is now down to four. I doubt they survive. Some 20 metres away is a cafe that we would frequent. It was good and busy (though too expensive). Inexplicably, and without explanation, it closed a few months ago and remains vacant. The former NAB building itself is a ghost of its former self, I do see people enter and leave but infrequently. I really don’t know that the building is worth the better part of a billion dollars.

Over in Europe it’s a similar story. Ghost offices and as you will read later the ECB is a leading light in exactly why that is the case.

Is it not obvious though? People voted with their feet. They don’t want to be in the office 5 days a week. That must surely be one of the payoffs of technological progress. Five days of commuting is hugely wasteful to time, to energy, surely there is an easy climate pay-off too. You see it everywhere, Monday is dead, Friday is dead, anytime it rains the city is dead.

In the UK, the Office of National Statistics has voted to strike about plans to require staff to be in the office 40% of the time. So not even half the time in the office and there is industrial action. German software giant SAP had a similar mutiny earlier in the year.

When it comes to ‘obvious stuff’, I view commercial real estate as obvious. Everyone I know close to it tells me it will bounce back like it always has before. They are the experts and maybe it will. Personally though I liken it to scenarios where I have a good idea and say to my children:

“Why don’t we do [good idea]?”

“Nah, don’t want to.”

Then it doesn’t happen, however much I wish for it and however invested in the idea I am. Why? Because they just don’t want to. Similarly, commercial real estate relies on people wanting to come to the office. They voted and they don’t want to, however much you might wish it.

Euro-Trash

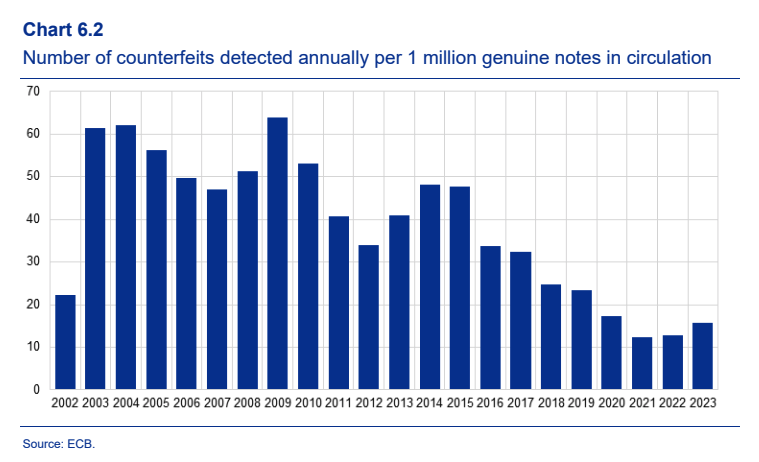

The ECB Annual Report was out last week. At 195 pages in length it's a tribute to opacity. In the bowels though there are some interesting things. Counterfeit notes steeply in decline, mirroring I suppose the continued shift to digital payments. It must simply no longer be as profitable because getting rid of the notes when you have printed them is harder than it was. Interesting trend.

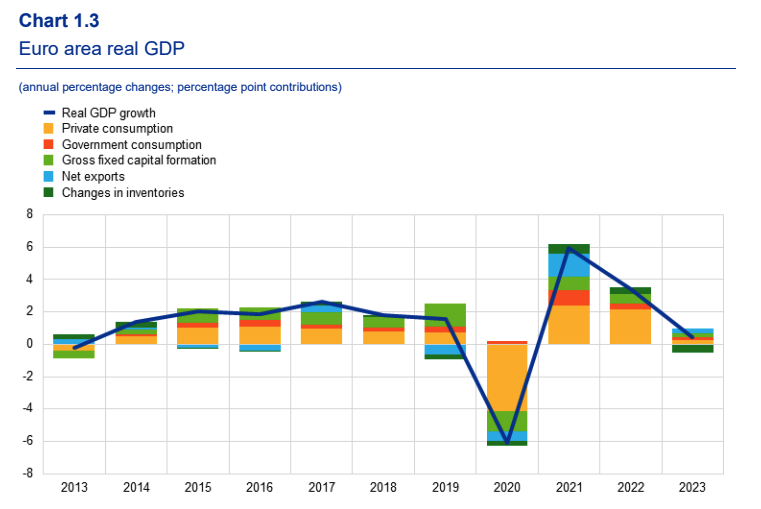

Also evident is the total stagnation of the European economy. After the covid trough and peak, it has gone nowhere with real growth barely exceeding 2% at any point in a decade managing only 1.3% in 2023. It’s an appalling economic performance which in reality is probably much worse.

Inside the bank itself, staff continued to accrue their giant defined benefit pension schemes. With an unprecedented 25% contribution rate from the bank. No need to worry about GDP if you work for the ECB. Aside from that there are new working conditions too.

There are 250 working days a year in Frankfurt and 13 public holidays (excluding any additional bank holidays). So it looks like a rough requirement to be there half the time.

I’m pretty sure that trend continues as well such that in 50 years looking back at an office culture where everyone had to sit in a little cubicle in a city where they don’t live will look cruel and unusual. Once a policy like this is instituted it's very hard, particularly in the public sector, to reverse it.

There is a clue for commercial real estate here. Maybe it does recover but personally if the ECB policy is any guide, I don’t see how.

Further information

Our April 2024 report to investors can be found here.

If you are considering an investment in the Managed Fund, you can apply using our online application form: