- MoneyBits

- Posts

- Since 1184

📚️ PDF⏳️ 6 min 📖 8

Bitcoin

A whole week of positive ETF inflows last week. The S&P 500 fell 2.2%, and gold dropped 3% and bitcoin gained over 10% as the crypto market added over US$200B. Why? As with all markets, we don’t really know. But the following ideas are true and may well be contributing.

Wars are expensive. Generationally expensive, amplifying debt and adding to inflation. Bond yields everywhere rose sharply last week as markets priced in more of both.

You can’t blow up Bitcoin. It sounds flippant but it is not intended to be. Distributed systems are far more resilient to war, than other assets. Lots of asset classes have single points of failure. Airlines with their susceptibility to oil prices are a good example, airports are an even better one. Entire continents could fall into the sea and bitcoin would keep going.

The general vulnerability of the economy to any sort of disruption is being laid bare in Iran and it begs the question, how resilient is your system?

Now the boring bit. The bit everyone hates when I talk about the Sovereign Individual (again). In that book they accurately predicted that wars would become incredibly expensive to prosecute as time went on, because the cost to smaller nations of doing enormous damage to larger ones would fall significantly. The concept was described as the “falling returns to violence”. Essentially, it costs very little now to cause great economic damage as the $10,000 drones hitting Dubai airport prove. Even worse, they are being shot down by $400,000 anti-drone missiles. It is a huge cost asymmetry.

It’s such a big issue in fact that the US Navy has its lead aircraft carriers (very sensibly) a long way back from the battle zone because they are so easy to attack with cheap weapons. The Houthis aren’t exactly renowned for their technological capability and yet can somehow threaten a vessel that carries more firepower than every nation on earth save for its host.

Save yourself the trouble of reading the book. This summary is good. The book improves with age, written in 1997 its predictions are becoming increasingly spooky.

“The biggest opportunities come from new niches created by exponential tech shifts and others’ failure to adapt.”

1000 years of history dies

So says the Electoral Reform Society. The United Kingdom’s Parliamentary system is a little odd in that until 1992 there were 600 members of the House of Lords who held hereditary peerages. Simply unelected barons who would lob up at the gates of parliament and be let in by dint of birthright.

84 hereditary peers remained until this week when they were voted out of existence. It must be said that most people are not sad about this at all. It's difficult to justify. Even so, if something survives a very long time in a hostile environment, it's probably quite a good idea.

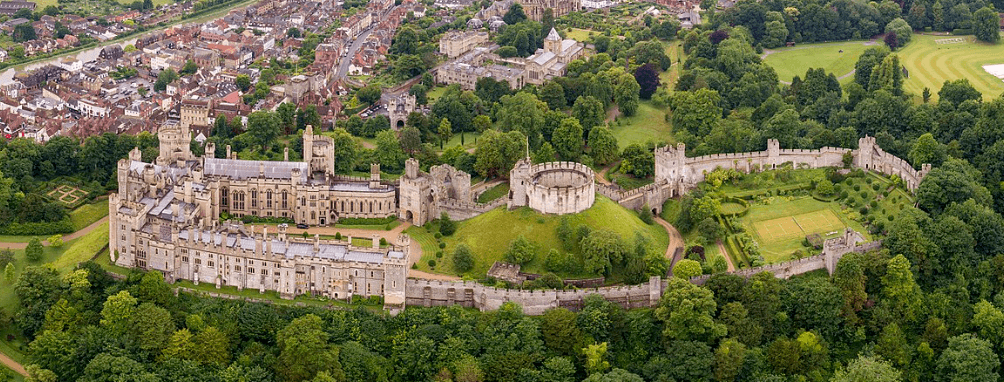

The oldest of this week's abolished peerages belongs to the Earl of Arundel. The family has held a continuous position in the House of Lords since 1184. They still live here, in Arundel Castle.

They also held the position of Earl Marshal meaning they oversaw the State Opening of Parliament as well as Royal Weddings and Funerals. No longer, the role will now be fulfilled by Brian, from Accrington.

What arguments are there for why this could be a good system? Well perhaps the only one I can advance is this: their legacy is inherited by their children. So they work quite hard to protect it and do the right thing. If such a thing exists they are ‘dynastically committed’. Also, because of the hereditary nature of the peerage, the children can’t really avoid what's coming their way either. So everyone needs to behave with reasonably good intentions. That does not always happen, but it is a good counterpoint to the alternative which is an entirely elected upper house who behave like tomorrow does not exist.

A case in point, Nancy Pelosi of the United States House of Representatives, a lifetime politician earning $200k, is somehow worth $400 million. I accept that she is an excellent stock picker but she has made Warren Buffett look like an amateur and she's not alone. There is disproportionate success in the US Senate too that defies probability. I’m not against their success, I just cannot explain it.

The fact is that the hereditary peerage is designed to avoid corruption. The consequence of misbehavior cascades through multiple generations. As a result, they broadly did behave and did not interfere with the work of the government if they did not have to.

It’s indefensible really but somehow it worked, and now it’s gone. It is possible that the system was cleverer than we thought it was and we will only find out once it is no longer there. It won't take 1000 years to find out either.

Slowly then, the nation state decays. It dismantles its infrastructure and consumes itself through spending.

Yields

The UK has been hit hard in terms of borrowing costs since the commencement of action in Iran. Rather surprising because they have been very reluctant to help out their closest ally. There is more to it and perhaps it’s because the natural response in the UK to any incident is to give away more money.

Barely a rounding difference £53m, 80 pence per resident. But the point is the spending continues and never seems to stop. In the last financial year the UK’s budget deficit was a massive 5.2% of GDP. The UK’s thirteenth largest since 1948. Annual borrowing is now around £2,200 per head of the UK’s population (or more importantly, £4,500 per private sector worker).

The situation was slightly less bleak in America where at least strong economic growth gives them a fighting chance but even then the bond market is not happy.

We have been promised a bond market reckoning forever. It will never come though. We know that from Japan. It can always be resolved by the magic money printer, and it always will be.

Total interest cost in the UK now £120 billion annually. Twice what is spent on defence and the equivalent of the entire education budget, and rising.

As we stand the Bank of England holds 8% of all outstanding gilts from its QE program. Quite soon, that number will begin to rise again.

Private credit

Is there another kind? Turns out that any lending not from a commercial bank is considered ‘private credit’. It's a very dark descriptor that I imagine was invented by the banks themselves to draw a shadow over markets in which they couldn’t, or wouldn’t, participate. Now private credit is big, and the question is, is it too big to fail?

March 16 (Reuters) - Private-credit market jitters have spilled onto Wall Street, with some major U.S. banks tightening lending while the funds have capped withdrawals as mounting concerns prompt firms to curb risk and brace for further strain.

Sentiment had been dented by concerns over valuations and transparency, as well as cases such as the bankruptcy of auto-parts supplier First Brands and car dealership Tricolor, where some private-credit lenders held exposure.

There seems to be tremendous drama in private credit because there are no strict requirements for funds to mark their investments to market. So if they lend $100 to something wobbly, it’s worth $100 until the day it’s worth zero.

We discussed this the other week in the context of commercial property. Most assets don’t actually need to find a price until they really, really need to find one. When that happens the price isn’t the price you thought it was. As a consequence, some private credit funds have restricted withdrawals because their assets can’t be sold, ‘temporarily’, of course.

For us, we suffer every downturn because bitcoin and ethereum and the rest have such visible pricing. Everyone knows exactly the price at all times:

“I see that bitcoin is down blah per cent”.

“Yes, you are exactly correct, to within cents. May I inquire as to the specific performance of your private credit investments?”

Bitcoin has more trading hours under its belt now than the NASDAQ itself. It's exhausting. Sometimes I just want a day off. 365 days 24 hours for all of those days always knowing the price.

We always, always know the price.

So much of the investment world is not like that because the price is probably some fraction of what the books say, but the rules are ok with that. For now.

Euro-Trash

As markets go digital? Surely they have been digital for 30 years or more. Payments in Europe using the SEPA system are already instant, you pay anyone in any Euro country via SEPA (which is free) and they receive their money instantly. What then is the Digital Euro for? Quite honestly I do not understand it but the ECB is pushing their Digital Euro Project really hard.

The arguments here were made in a podcast by Piero Cipollene, an ECB Board Member.

We’re back on the whole ‘Blockchain’ thing again. Blockchain good, bitcoin bad etc. Fundamentally, at its core it completely misunderstands the technology. Blockchains are intentionally designed to be slow. The reason is so the person in Peru and the one in Mongolia can download data within the same fixed window and have a reference point that they can both agree on. Bitcoin arbitrarily chose 10 minute windows for that purpose. It’s slow because it controls for slower bandwidth and geography because everyone has to host the software.

You would never run a ‘blockchain’ if you were the only person that could write to it, which is exactly what the ECB proposes. It just does not make any sense. They should use an Oracle database like every other big player in the world does.

The whole thing is a mad salad of nonsense verbiage.

The full roadmap can be found here. I wish you the very best of luck if you choose to read it. All I took from it was this:

“With Appia, the Eurosystem aims to deliver a blueprint for a future long-term solution by 2028, in cooperation with both public sector and market stakeholders”

What?

Two years to come up with just a blueprint for a future long-term solution.

Further Information

Our February 2025 report to investors can be found here.