- MoneyBits

- Posts

- Wrong again

📚️ PDF⏳️ 7 min 📖 6

One article

I worked for a menial's hire,

Only to learn, dismayed,

That any wage I had asked of Life,

Life would have willingly paid.

This article caused ructions across the globe this week. Over 300 million views. It was a rather doomsday scenario about what is happening with the continuing acceleration of general intelligence. There were lots of targets for doom. One of them, perhaps the one causing the most financial impact, was the credit card interchange fee, which has always been a rip off. The thesis was

“AI Agents will eventually transact on Stablecoin payment rails and bypass interchange”

It caused significant declines in some major financial players, because the AI robots are going to choose digital money and refuse to pay interchange. Of course they are.

Most of us do not understand or care about the interchange fee. If you buy something for $5, you pay $5. It is the merchant that bears the interchange, an invisible racketeering layer between the banks and the card companies. It is deliberately opaque and a constant target for regulators. Who can be bothered though to change the payment rail anyway for such a small amount? The answer is AI. Nothing is boring for AI. If it is handling your payments, it isn’t going to want to pay interchange, which it does understand, so the ultimate outcome will be you pay less.

There was more drama in the article too about white collar job losses, the doom loop of lower spending capacity and financial collapse etc. Maybe. Technology though has never made us poorer, ever. It certainly reallocates though, horse cart manufacturers stopped doing as well as Henry Ford but overall things got better.

If the technological acceleration means the price of things falls from $100 to $90 but my income falls from $200 to $150 then it is very bad for me. But your $50 decline went somewhere, someone is shelling out less and keeping the $50.

That’s the game then, overall wealth up but pretty surely not evenly distributed.

You could ask your ClawdBot agent what it thinks you should do, over time it will get to know you well. If you don’t know what I’m talking about then it might be a good moment to watch this video and have a go at installing one. Be very careful. Build something very simple and do not install it on your main computer.

If you are depressed by the first article. Refresh yourself with this much more positive view. Abundant intelligence, up and to the right. All you have to do is engage, and actually it requires what I would call “enjoyable effort”. All you need to do is ask for what you want. Then your agents build it for you and you sit back in awe.

Across the world, almost nobody is doing it. Completely blank canvas.

It is entirely true now to say that by next week you could have the equivalent of 20,000 people working for you. It would be a significant technical effort, but it can be done and one red dot represents the number of people having a go.

In the reallocation of economic gains, where do you think they are going to go?

Getting windy

In the UK between 2009 and 2024, installed generating capacity increased by 20.7%, yet electricity output fell by 24.2%. Every growing economy grows power production. There is no other way.

It is a significant drop in the efficiency of the UK’s power network. It closely tracks the relative decline of the UK’s GDP versus the rest of the world. In fairness to the politicians that delivered it, the UK did vote for this and a lot of people consider it a significant success story.

You can map the wealth of nations though from TWh/Capita straight to GDP. The UK was a 6 TWh/person economy, now it is 4.6 TWh/person (and dropping).

China is at 5.1 TWh/person economy (and rising). Japan, 8.15 TWh/person. The US is a whopping 12 TWh/person (and starting to rise again). It actually feels about right.

Incidentally, the bitcoin network consumes 200TWh annually, two thirds of the UK consumption and growing.

The power is the money. Everything else is a story.

Commercial Property

I wonder about the continued renaissance of commercial property. In particular, I often see articles in the Financial Review spruiking a ‘comeback’. The 33rd comeback since Covid. The articles are written by experts of course and I know very little about commercial RE, I’m sure lots of the sector is doing really well. Data centres in particular.

A case in point. SalesForce Tower Sydney. 99% occupancy. But honestly, look at the view. It must be one of the greatest views in the world, if not the greatest. Of course that office is full. It will be full right up until someone builds in front of it in 30 years. But really, is that indicative of the wider market?

300 metres away, a commercial office has been dormant for five years. Across the corridor from us a 70 seat office has been empty for a year. The ‘return to office’ mantra is very real except that people don’t want it. It’s a meaningless sample size but the length of the dormancies near us is shocking. Sure, everyone wants the showcase office on the top floor to impress clients, but two blocks away the story is different.

The battle for “come into the office” is lost. Employers just outright lost that one. People actively select roles that allow flexibility, they will accept significantly less money for flexibility too because going to the office isn’t free. I guess $50/day at least in time and extras.

Commercial property needs to drop 20% just to accommodate one day a week at home (it has). Now it’s under pressure because of artificial intelligence. Claude Code does not need a chair, so surely more pressure?

One of the reasons I think that so much positivity surrounds the industry is the presence of the big Super Funds. Some 20% of office space in Australia is owned by them. It suits nobody if these funds do not perform well, everyone in Australia is invested in CRE going well either directly or indirectly.

It seems to me an asset that is hard to price. Your mates at Lunch & Lunch Valuations pop in every three years and off we go. It doesn’t have to engage with the day-to-day variability of price visibility. As a consequence, how robust is it?

There is something to be said for having an active market price trading 24/7 365 days a year. It doesn’t do much for weekend relaxation but it is absolutely robust and the more you survive in that market, the more you survive.

Great views from the top floor will draw yield forever, but when the cold winds really blow on CRE, will it find a price?

Wrong again

Last week I confidently predicted that nobody would admit to sacking people because of AI. “Nobody would dare”.

Enter Richard White of WiseTech this week, whose CEO proudly proclaimed that 2,000 people would be sacked because “the era of manually writing code is over”.

The Commonwealth Bank was more measured. After last year's debacle where they were going to sack 45 people because of AI and didn't. They have spent $90 million on a new site to help employees ‘transition’. The goal is “transparency and opportunity”, prior to near certain death. In 2025, you were getting sacked. In 2026, there is a website to help explain exactly why you will be sacked in 2027. On balance, I suppose it is better.

Anyway, it was coming. Now it is here and I was wrong about people not saying so. Now that somebody has, there might be more confidence from others to do the same.

That is to say, actually tell the truth.

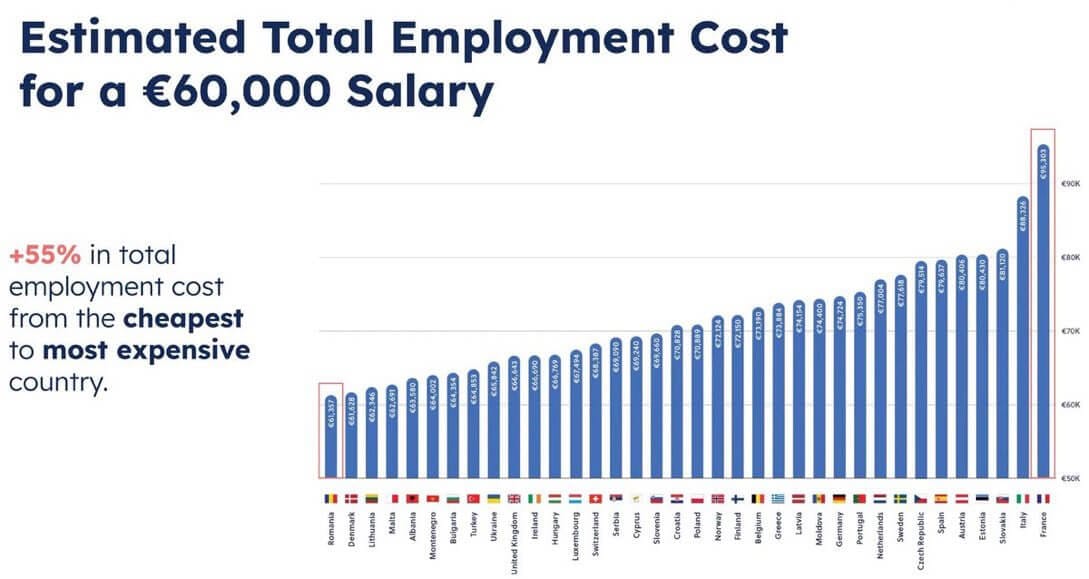

Euro-Trash

As we have covered before, to pay someone €60,000 in France costs €95,000. There are all manner of on-costs and employer taxes that make up the amount and overall, if you have a job in France it is an excellent outcome. In fact, the ideal job in France is to work for the government in a senior role, but not so senior that you might be the victim of political fall-out. “Invisibly senior”, is where you need to be. Deputy under-director of regional procurement is what you should be aiming for.

The problem with the arrangement though is you get this. The official European statistics on new businesses versus bankruptcies in Europe. A net loss of about 80,000 businesses a year. Which nearly fully explains why the French state is 60% of the economy and why every economy in Europe has an exploding public sector.

There is a pretty clear trend across most of Europe to bigger government, which is perhaps why the German Finance Minister stepped up this week to rule-out joint Euro-Bonds.

“As German finance minister, I will always stand for stability,” Klingbeil acknowledged that the debate around Eurobonds is evolving and pointed to the more “nuanced” comments recently made by Deutsche Bank CEO Christian Sewing and Bundesbank President Joachim Nagel. Notably, Nagel has softened the Bundesbank’s traditional opposition to joint EU debt. Nevertheless, Klingbeil stressed that “the position of the federal government remains unchanged,” arguing that there is currently no need to shift course as sufficient EU funds are available. The remarks highlight a clear divergence between the Federal Ministry of Finance and the Bundesbank in this increasingly important debate.

Well, guess what? Herr Nagel is not getting the ECB President's job if he says he is opposed to joint Euro-Bonds. So he pretty much has to say he isn’t. Helpfully, the Finance Minister has no such pressures and can simply rule them out.

These are not trivial off the cuff remarks. The Germans want Nagel in the ECB chair. Whatever he needs to say to get there, he will say. If he gets there, I bet a Deutsche Mark he has a subtle shift of position.

The French are bankrupt. The Germans are not. All to play for as regards Christine Lagarde’s hot seat.

Further Information

Our January 2025 report to investors can be found here.